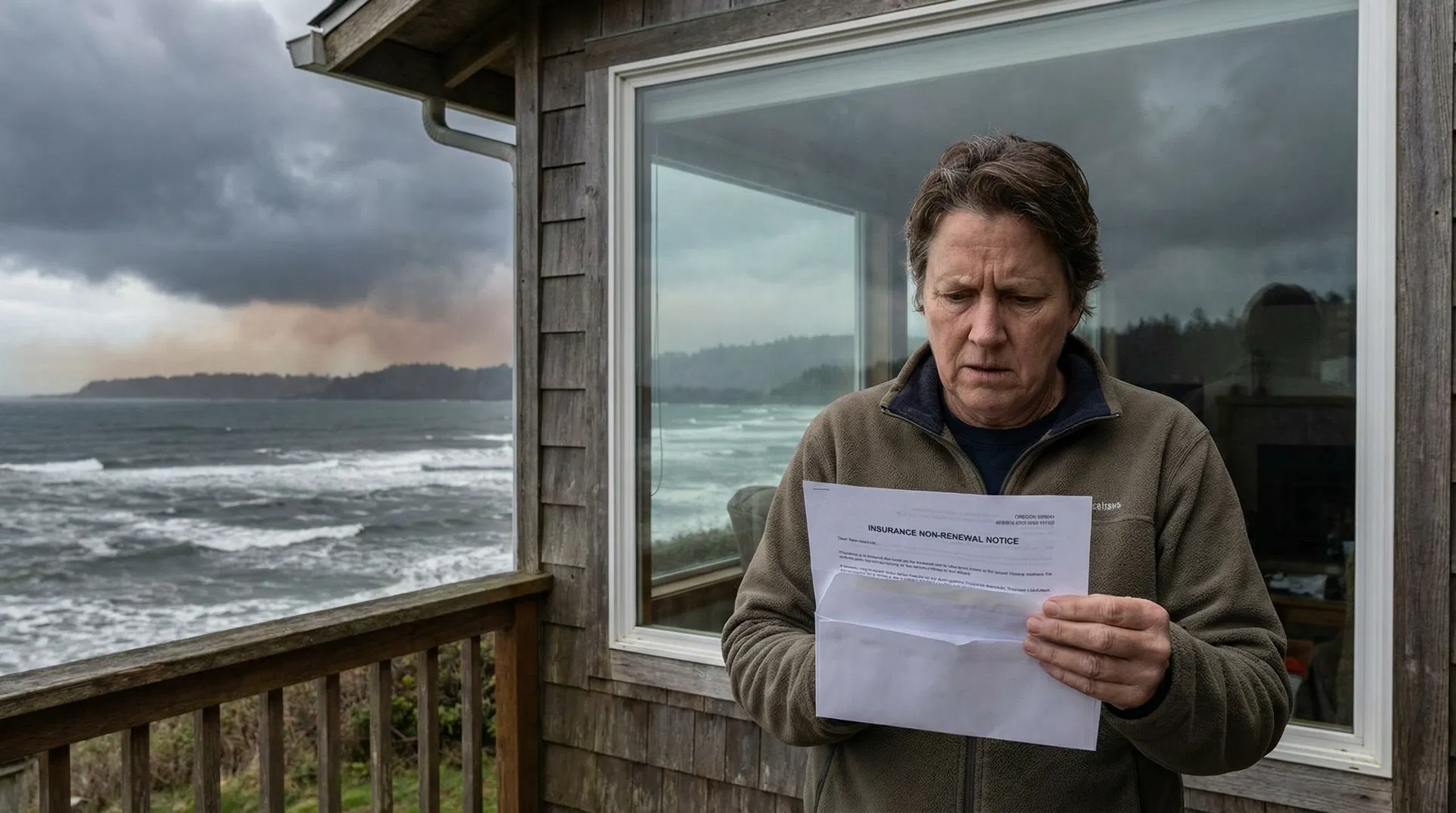

If you have received a homeowner's insurance non-renewal notice in the mail, you are not alone — and you are not without options. Across the Oregon Coast and throughout Oregon's wildfire-prone regions, insurance carriers are pulling back from high-risk areas, leaving thousands of homeowners scrambling to find replacement coverage. Here is what you need to know and what you should do right now.

Act Immediately — Do Not Wait

Oregon law requires carriers to give you at least 30 days notice before non-renewal. But finding replacement coverage in a tight market takes time. Contact Gerald Ross Agency as soon as you receive a non-renewal notice — do not wait until your policy is about to expire.

Why Are Carriers Non-Renewing Oregon Homeowner Policies?

The primary driver of non-renewals in Oregon is wildfire risk. After years of catastrophic wildfire losses in California, Oregon, and other western states, many major carriers have concluded that the risk in certain areas is simply not profitable to insure at standard rates. Rather than dramatically raise premiums (which is politically and regulatorily difficult), many carriers are choosing to exit high-risk markets entirely.

This is not a reflection of your personal claims history or your creditworthiness — it is a portfolio-level decision by the carrier based on the geographic risk of your property's location. Carriers are using increasingly sophisticated wildfire risk modeling tools that score individual properties based on factors like proximity to wildland vegetation, slope, aspect, historical fire frequency, and local fire suppression resources.

Your Step-by-Step Action Plan

- Step 1: Don't panic: A non-renewal notice does not mean you are uninsurable. It means your current carrier has decided not to continue your policy. Other carriers may still be willing to write your home.

- Step 2: Contact an independent agent immediately: An independent agent like Gerald Ross Agency works with multiple carriers, including specialty and surplus lines carriers who continue to write in high-risk areas. We can shop the market on your behalf.

- Step 3: Document your mitigation efforts: If you have made home hardening improvements (Class A roof, ember-resistant vents, defensible space), document them with photos and receipts. This can significantly improve your insurability.

- Step 4: Consider the FAIR Plan as a last resort: Oregon's FAIR Plan provides basic property insurance to homeowners who cannot obtain coverage in the standard market. It is more limited and expensive than standard policies, but it ensures you are not left uninsured.

- Step 5: Review your coverage needs: This is also a good time to review whether your current coverage limits are adequate. Many Oregon homeowners are significantly underinsured — your home's replacement cost may be much higher than your current policy limit.

Specialty and Surplus Lines Carriers: Your Best Option

When standard carriers decline to write a property, specialty and surplus lines carriers often step in. These carriers are specifically designed to handle risks that fall outside the standard market's appetite. They typically charge higher premiums than standard carriers, but they provide genuine coverage — not the stripped-down protection of the FAIR Plan.

As an independent insurance agency, Gerald Ross Agency has access to specialty and surplus lines markets that are not available to captive agents or directly to consumers. We serve homeowners throughout the Oregon Coast, including Gold Beach, Bandon, Coos Bay, and Newport.

How Home Hardening Can Help You Get Covered

Many specialty carriers will write policies for high-risk properties if the homeowner has taken documented steps to reduce their wildfire risk. Home hardening improvements — Class A roofing, ember-resistant vents, non-combustible decking, and maintained defensible space — can significantly improve your insurability and may reduce your premium even in the specialty market. See our guide on wildfire insurance and home hardening for a complete checklist.

Received a Non-Renewal Notice? We Can Help.

Gerald Ross Agency works with specialty carriers who continue to write homeowner policies in Oregon's high-risk wildfire areas. Contact us today — don't wait until your policy expires.